This week, the total inventory of construction steel continued to decline, with rebar inventory down 2.20% WoW and wire rod inventory down 2.70% WoW. Supply side, EAF steel mills saw further declines in operating rates due to difficulties in steel scrap procurement and worsening losses. According to an SMM survey, the operating rate of 50 EAF steel mills specializing in construction materials nationwide stood at 34.64%, down 3.78% from the previous period. For BF steel mills, profits remained, but some mills gradually arranged production cut plans amid news of crude steel output reductions and the transition to the off-season. Per SMM's weekly maintenance survey, the impact from maintenance on construction materials reached 1.1378 million mt this week, up 24,000 mt WoW, indicating a notable overall supply reduction. Demand side, high temperatures persisted in north China, while south China entered the rainy season, limiting construction progress at downstream sites. Just-in-time procurement was maintained overall, though the purchasing pace slowed slightly, reflecting weak demand. Under this weak supply-demand balance, construction steel inventory continued to decline at a relatively steady pace.

This week, total rebar inventory stood at 5.2603 million mt, down 118,300 mt WoW (a 2.20% decline, previous: -1.82%), and down 1.9764 million mt (27.31%, previous: -26.24%) compared to the same lunar period last year.

Table-1: Rebar Inventory Overview

Data source: SMM

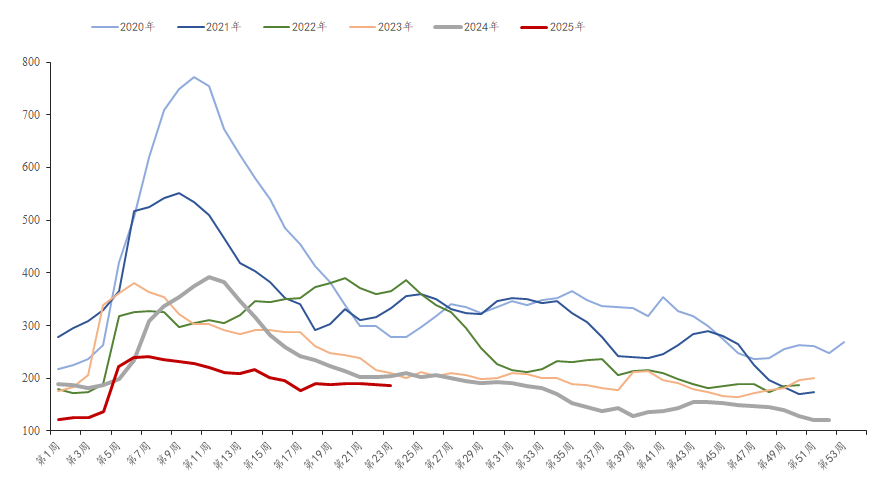

This week, rebar in-plant inventory totaled 1.8602 million mt, down 21,100 mt WoW (a 1.12% decline, previous: -0.89%), and down 169,000 mt (8.33% YoY decline, previous: -10.64%) compared to last year. Combined supply cuts from BF and EAF steel mills and normal direct mill shipments led to continued inventory declines, with the pace slightly accelerating.

Chart-1: Rebar In-Plant Inventory Trend, 2020-2025

Data source: SMM

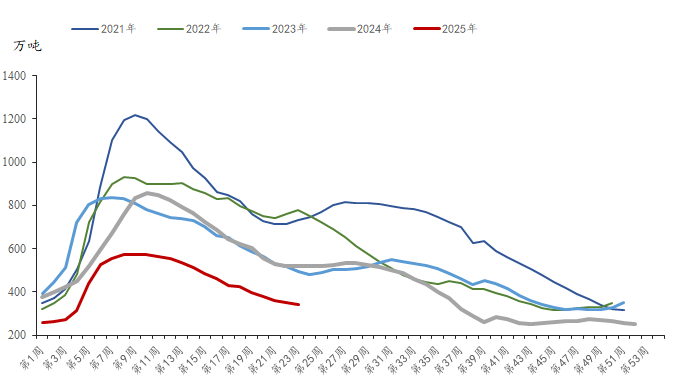

This week, rebar social inventory stood at 3.4001 million mt, down 97,200 mt WoW (a 2.78% decline, previous: -2.31%), and down 1.8074 million mt (34.71% YoY decline, previous: -32.58%) compared to last year. Although futures prices edged up slightly, traders remained cautious, mostly opting to sell at lower prices. Meanwhile, end-user sites maintained just-in-time procurement, driving further declines in social inventory.

Chart-2: Rebar Social Inventory Trend, 2021-2025

Data source: SMM

Overall, construction materials face weak supply and demand. Considering persistent heavy rainfall in south China and continued high temperatures in north China, demand is expected to weaken further marginally. Meanwhile, macro-level uncertainties persist amid China-US talks, limiting upward momentum for construction material prices. With insufficient end-use demand resilience, total inventory declines are likely to narrow next week, and inventory buildup may occur if demand remains weak.

![Before the holiday, the black chain is unlikely to see a trend-driven market [SMM Steel Industry Chain Weekly Report].](https://imgqn.smm.cn/usercenter/zUFfM20251217171748.jpg)

![[SMM Chromium Daily Review] Inquiries and Transactions Weakened, Chromium Market Showed Mediocre Performance Before the Holiday](https://imgqn.smm.cn/usercenter/ENDOs20251217171718.jpg)